Unmanned Warriors: How Military Robots are Redefining Defense Capabilities

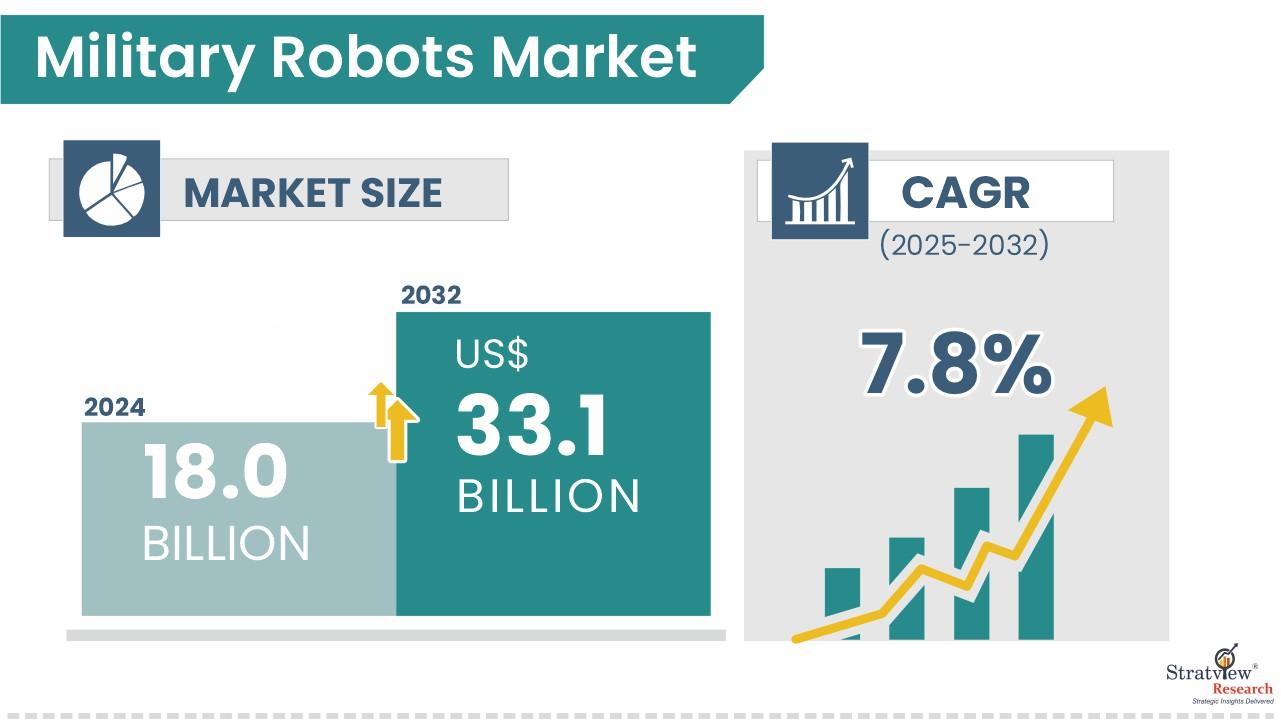

Military robots encompass a broad set of unmanned systems—ground, aerial, marine—used for multiple defense tasks like ISR, logistics, EOD, combat support, and more. Stratview Research estimates the military robots market at USD 18.0 billion in 2024, growing at around 7.8% CAGR through 2025-2032, to reach USD 33.1 billion by 2032. As technologies evolve and threats change, military robotics is becoming a core element for strategic capabilities.

Request the Sample Report Here:

https://www.stratviewresearch.com/Request-Sample/2913/military-robots-market.html#form

Drivers

- Geopolitical tensions & shifting defense priorities: Nations facing border disputes, asymmetric threats (terrorism, insurgency), or competition in maritime and aerial domains are investing in robotics to enhance operational reach and flexibility.

- Technological enablers: Improvements in autonomy, AI, sensor payloads (cameras, radar, thermal, lidar), secure communications, and power systems (battery, energy management) enable better robot performance.

- Cost and efficiency demands: Using robots for tasks that are dangerous, monotonous or would require high human risk helps reduce costs over time, reduces casualties, and allows forces to deploy human operators where uniquely necessary.

- Operational demand for ISR & surveillance: As real-time intelligence becomes more critical—especially in contested zones—military forces demand persistent surveillance, which unmanned platforms can deliver more safely and efficiently than manned ones in many cases.

Trends

- Autonomous & semi-autonomous systems increasing: More systems are being developed that require less human control, able to make certain decisions on their own under set rulesets (e.g. route navigation, obstacle avoidance, target recognition).

- Proliferation of small, attritable systems: Smaller robots, swarms, expendable UAVs/UGVs that can be deployed in quantity are getting attention. Such systems accept that some units will be lost, so cost per unit and rapid replaceability become design factors.

- Sensor & payload enhancements: Better imaging, infrared, thermal sensors, electronic warfare (EW) payloads, as well as multi-sensor fusion (combining vision, radar, lidar etc.) are being integrated for better situational awareness, target identification, and environmental adaptation.

- Regulatory, ethical, and export constraints: Fully autonomous lethal robots are under scrutiny; export controls, technology sharing restrictions, and ethical rules (human-in-the-loop) are limiting scale or adoption in some regions.

Conclusion

The military robots market is on a strong upward trajectory, driven by rising military expenditure, requirement for force protection, and fast-moving tech in autonomy, sensors, and unmanned systems. From USD 18.0B in 2024 to USD 33.1B by 2032, the path ahead offers sizeable opportunity.

Challenges remain: ethical and legal boundaries, technical durability and reliability in harsh and contested conditions, secure communications, power supply and autonomy constraints, cost pressures, and the changing regulatory landscape. Stakeholders who can balance cutting-edge performance with operational viability, ethical constraints, and cost will be best placed. Market leaders, especially in North America and emerging centers in Asia-Pacific, will likely shape the future of military robotics.