Strategic Outlook in the Construction Films Market: Opportunities & Challenges

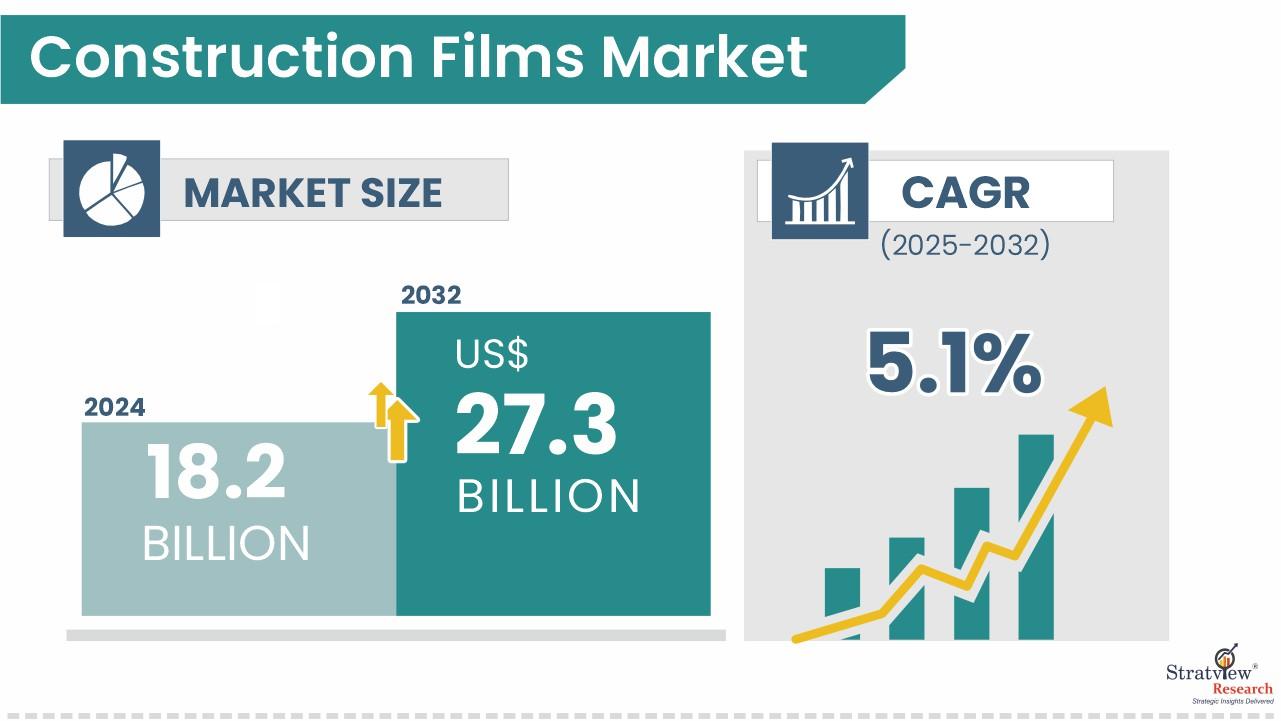

For those in building materials, construction, or polymer film production, the construction films market offers a compelling opportunity. Stratview Research projects this construction films market to grow from USD 18.2 billion in 2024 to USD 27.3 billion by 2032, growing at 5.1% CAGR over 2025-2032. This growth is being shaped both by demand pressures and evolving regulatory, environmental, and material innovation trends.

Download the Fee Sample Report Here:

https://www.stratviewresearch.com/Request-Sample/671/construction-films-market.html#form

Drivers

- Demand from residential, commercial, and infrastructure sectors: As cities expand and infrastructure projects accelerate, so does the need for construction films for protection, insulation, vapor/moisture control, temporary covers, and finishing works.

- Regulatory / Standards push for energy efficiency & green construction: Building codes and green building rating systems are increasingly requiring better moisture vapor protection, better insulation, and materials that contribute to energy efficiency. Films play a role in enabling compliance with those.

- Focus on durability & performance: Films that resist UV, moisture, tear, and environmental wear are more in demand. Also, cost efficiencies related to lifespan, fewer replacements or damage repairs drive usage.

Trends

- Material diversification and innovation: LLDPE is leading, but other materials (HDPE, PET/BOPET, PP, PVC, etc.) are used for specific performance requirements (strength, clarity, UV resistance, decorative appearance).

- Protective & barrier films dominate the use-case: While decorative / aesthetic films are used (for coverings, decorative surfaces), protective and barrier applications (vapor, moisture, dust, etc.) are where most demand is, especially in newer buildings and infrastructure.

- Asia-Pacific pulling ahead: With high construction volumes, lower labor costs, industrial scale, and supportive government infrastructure/investment, Asia-Pacific leads and is expected to grow fastest. China and India are especially central.

Conclusion

For stakeholders—manufacturers, film producers, construction contractors, distributors—the construction films market represents a stable growth sector. As demand shifts toward performance, durability, regulatory compliance, and sustainability, firms that invest in better film materials, eco-friendly manufacturing, and high-performance barrier/protective functionalities will be well positioned. Moreover, positioning in high-growth markets (Asia-Pacific) and ensuring cost-effectiveness (both in production and logistics) are likely to yield competitive advantage. While competition is strong, the expanding market size (USD 27.3B by 2032) offers room for innovation, differentiation, and scale.