Global Data Center RFID Market Forecast: Growth Trends, Segmentation, and Insights

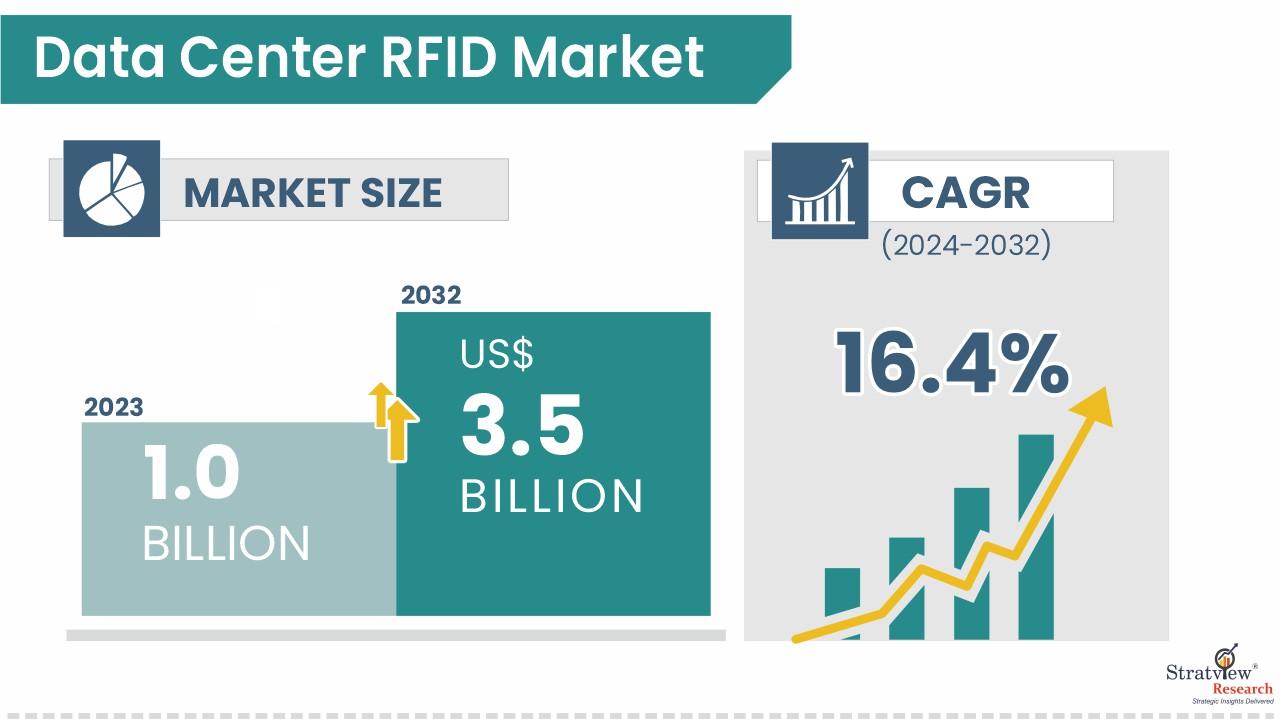

The Data Center RFID Market was USD 1.0 billion in 2023 and is likely to reach USD 3.5 billion by 2032. The market is expected to grow at a CAGR of 16.4% during 2024-2032.

The report highlights key insights related to the data center RFID market size, trends, and future market growth and forecast, along with the competitive landscape and emerging opportunities. It is designed to help stakeholders understand market direction and make data-driven decisions.

The Data Center RFID Market is gaining momentum as operators seek stronger asset visibility across increasingly complex facilities. A key structural growth driver is the expansion of hyperscale and colocation environments, where automated tracking, audit readiness, and infrastructure visibility directly improve operating control and reduce manual errors.

“The Data Center RFID Market is expected to grow at a CAGR of 16.4% during 2024-2032.”

Request a free sample report: https://www.stratviewresearch.com/Request-Sample/4595/data-center-rfid-market.html#form

Market Segmentation Analysis

Data Center RFID Market is segmented by Application Type (IT Asset & Infrastructure Tracking, Security Access & Compliance Management, and Environmental & Operational Monitoring), by Tag Type (Passive, Semi-Passive, and Active), by Reader Type (Fixed Reader and Handheld Reader), by Frequency Type (Low Frequency, High Frequency, and Ultra High Frequency), by Data Center Type (Hyperscale, Colocation, Enterprise, and Edge) and by Region (North America [The USA, Canada, and Mexico], Europe [The UK, Germany, France, and Rest of Europe], Asia-Pacific [China, Australia, Japan, India, and Rest of Asia-Pacific], and Rest of the World [Brazil, Africa, and Others]).

By application type, IT Asset & Infrastructure Tracking leads the market, while Environmental & Operational Monitoring is the fastest-growing segment. The leading position of IT Asset & Infrastructure Tracking comes from the need for automated inventory controls, lifecycle tools, and audit records across hyperscale and colocation facilities. Environmental & Operational Monitoring is expanding faster because sensor-based RFID tags support real-time condition monitoring and predictive maintenance in high-density settings. The strategic implication is clear: operators are moving beyond simple tracking toward broader operational intelligence.

By tag type, Passive Tag systems dominate current deployments, while Active Tag systems exhibit the fastest growth. Passive tags hold the largest share because they are low cost, battery-free, long life, and suitable for large-scale tracking across servers and racks. Active tags are growing faster because they support real-time location tracking and sensor-enabled environmental monitoring with longer reading ranges and programmability. This suggests that the market analysis is increasingly shaped by the balance between deployment economics and advanced monitoring needs.

By reader type, Fixed Reader installations account for the largest market share, while Handheld Readers show the fastest growth. Fixed readers are widely installed at entrances, cages, aisles, and storage areas to enable continuous automated asset tracking, movement tracking, and integration with access control and audit systems. Handheld readers are growing faster because they support field audits, exception investigation, and distributed facility management. This indicates that the industry outlook is shifting toward a mix of permanent monitoring infrastructure and flexible operational tools.

By frequency type, Ultra High Frequency leads both current installations and growth rates. UHF holds the highest and fastest-growing share because it offers the longest read range, fast scanning speed, and the ability to monitor bulk inventory and zone-level assets in large data halls. Its low-cost passive tags and EPC Gen2 standardization also make large-scale deployments more cost-effective. This strengthens the case for UHF as the preferred architecture in large and automation-heavy environments.

By data center type, Colocation facilities drive substantial RFID adoption, while Hyperscale data centers demonstrate the fastest growth. Colocation facilities benefit from RFID because multi-tenant asset segregation, service level agreement compliance, and automated inventory tracking are operational priorities. Hyperscale facilities are growing faster because their large infrastructure scale demands full automation, high-speed bulk scanning, real-time location visibility, and integration with advanced deployment systems.

Explore the latest market analysis and forecasts for the Data Center RFID Market: https://www.stratviewresearch.com/4595/data-center-rfid-market.html.

Regional Market Insights

North America leads the Data Center RFID Market. Its lead position is driven by concentrated hyperscale infrastructure, mature technology adoption, stringent compliance systems, and developed DCIM integration, with the U.S. at the center of adoption. From an industry insights perspective, this means RFID demand is closely tied to mature infrastructure environments where automation and governance are already embedded into operations.

Asia-Pacific demonstrates the fastest regional growth. The region is being propelled by aggressive digital transformation, data center construction programs, data localization policies, and growing hyperscale capacity, especially across China, Japan, and India. The market forecast for the region therefore reflects both greenfield buildouts and the need to embed asset visibility tools early in facility expansion cycles.

Emerging Trends Shaping the Data Center RFID Market

The market direction points toward deeper automation within data center environments. RFID is increasingly aligned with real-time visibility, predictive maintenance, and broader operational monitoring rather than basic identification alone.

Another important shift is the stronger role of sensor-enabled and programmable solutions. As infrastructure becomes denser and more distributed, users are prioritizing technologies that support both location intelligence and condition awareness. This is why active tags, handheld readers, and environmental monitoring functions are gaining pace within the wider market share evolution.

Key Growth Drivers of the Market

- Expansion of hyperscale and colocation facilities is increasing the need for automated asset tracking, because larger and multi-tenant environments require better control, compliance, and infrastructure visibility.

- Rising AI-driven infrastructure complexity is boosting demand for real-time asset visibility, as more equipment density and operational interdependence make manual tracking less effective.

- Regulatory compliance requirements are supporting adoption, because operators need stronger audit records, access control integration, and governance across critical facilities.

- RFID integration with DCIM and BMS platforms is improving operational efficiency, because connected infrastructure systems allow better monitoring, movement tracking, and decision-making.

- Expanding edge data center deployments are creating new demand, because remote sites need asset visibility and monitoring where on-site manual controls are constrained.

Competitive Landscape

Top Companies in the Market

- Avery Dennison Corporation

- Impinj, Inc.

- Zebra Technologies Corporation

- Honeywell International Inc.

- HID Global Corporation

- Eaton Corporation Plc.

- Fujitsu Limited

- Invengo Information Technology Co., Ltd.

- RF Code, Inc.

- NXP Semiconductors N.V.

Conclusion and Strategic Outlook

The Data Center RFID Market stood at USD 1.0 billion in 2023 and is projected to reach USD 3.5 billion by 2032 at a CAGR of 16.4% during 2024-2032. Growth is being supported by strong demand for automated tracking, compliance readiness, environmental monitoring, and real-time operational visibility across data center environments.

The strategic outlook remains tied to infrastructure scale and operational complexity. Leading demand is coming from North America, while Asia-Pacific is expanding the fastest, and the strongest segment momentum is visible in Environmental & Operational Monitoring, Active Tags, Handheld Readers, UHF systems, and Hyperscale facilities.

FAQs – Data Center RFID Market

1. What is the current market size and forecast for the Data Center RFID Market?

The Data Center RFID Market was valued at USD 1.0 billion in 2023 and is projected to reach USD 3.5 billion by 2032. The market is expected to grow at a CAGR of 16.4% during 2024-2032.

2. What is driving growth in the Data Center RFID Market?

Growth is being driven by hyperscale and colocation expansion, rising AI-driven infrastructure complexity, demand for real-time asset visibility, regulatory compliance requirements, and integration with DCIM and BMS platforms. These factors make RFID more valuable in modern data center operations.

3. Which region has the largest demand in the market?

North America holds the largest market share in the Data Center RFID Market. Its leadership is tied to hyperscale concentration, mature colocation infrastructure, technology leadership, and ongoing modernization cycles.

4. What does the investment outlook look like for this market?

The investment outlook appears favorable because the market combines a strong 16.4% CAGR with rising demand across both existing facilities and new data center builds. Faster growth in Asia-Pacific and hyperscale deployments also supports a positive industry outlook.

5. What are the main risks or constraints in the market?

The source page does not provide a dedicated list of market constraints. However, it does show that adoption patterns differ by application, tag type, reader type, frequency type, and data center type, which suggests deployment choices must align closely with operational requirements.