Is the Global Rubber Market Set to Grow Steadily at a 2.8% CAGR to Hit USD 39.13 Billion by 2034?

According to a new report from Intel Market Research, the global rubber market was valued at USD 32.45 billion in 2025 and is projected to grow from USD 33.52 billion in 2026 to USD 39.13 billion by 2034, exhibiting a CAGR of 2.8% during the forecast period (2026–2032). This steady growth is driven by expanding automotive production, infrastructure development, and increasing demand for durable industrial materials across key sectors.

What is Rubber?

Rubber is an essential elastomeric material prized for its flexibility, resilience, and durability. It exists in two primary forms: natural rubber, derived from the latex of rubber trees (Hevea brasiliensis), and synthetic rubber, manufactured through chemical polymerization. Natural rubber dominates high-performance applications due to its superior tensile strength and elasticity, while synthetic variants like Styrene Butadiene Rubber (SBR) and Nitrile Butadiene Rubber (NBR) offer specialized properties including oil resistance and thermal stability.

The global rubber market is expanding steadily, supported by strong demand from key industries such as automotive, construction, and manufacturing. Rubber is essential in applications ranging from tires and gaskets to footwear and industrial components, thanks to its durability, elasticity, and resistance to heat and wear. Synthetic rubber holds a major share of the market due to its consistent quality, cost-effectiveness, and wide usage across sectors.

📥 Download Sample Report: https://www.intelmarketresearch.com/download-free-sample/1828/rubber-2025-2032-839

Key Market Drivers

1. Automotive Industry Expansion Fuels Rubber Demand Growth

The continued growth of the automotive industry is a key factor boosting global rubber demand. Each vehicle produced requires a significant amount of rubber for components like tires, seals, hoses, and belts. With global vehicle production nearing 95 million units in 2024, the volume of rubber needed for both original equipment and replacement parts is substantial. The tire segment alone accounts for a major portion of rubber consumption, driven not just by new car sales but also by the consistent demand in the aftermarket sector.

Asia-Pacific, led by countries like India and China, plays a central role in this demand surge. In India, the majority of natural rubber produced is directed toward automotive use, particularly tires and tubes. While regions like North America and Europe also contribute significantly, global supply growth is lagging behind consumption, leading to tighter markets and price fluctuations.

With electric vehicles gaining momentum and vehicle production expanding globally, the demand for rubber both synthetic and natural is expected to rise further. To meet this growing need, manufacturers are increasingly focused on sustainable sourcing, material innovation, and supply chain efficiency, ensuring rubber remains a critical input for the evolving automotive landscape.

2. Infrastructure Development Accelerates Industrial Rubber Adoption

Rapid urbanization and construction activity in developing nations are driving demand for rubber products in building applications. Waterproofing membranes, vibration isolation pads, and expansion joints all utilize specialized rubber compounds. The global construction industry, valued at over $12 trillion annually, increasingly favors durable elastomeric materials for infrastructure projects. Recent government investments in public works programs across Southeast Asia and the Middle East are creating sustained demand for construction-grade rubber. Additionally, the growing prefabricated construction sector relies heavily on rubber components for modular building systems.

3. Sustainability Trends Reshape Material Preferences

Environmental regulations and corporate sustainability initiatives are reshaping rubber market dynamics. The EU's circular economy action plan has prompted innovation in eco-friendly rubber solutions, with recycled rubber content in new products increasing by nearly 30% year-over-year. Bio-based synthetic rubbers derived from renewable feedstocks now represent approximately 5% of total production, with major manufacturers investing heavily in green chemistry alternatives. Energy-efficient tire technologies that reduce rolling resistance are gaining market share as automakers pursue carbon neutrality goals.

Market Challenges

-

Raw Material Price Volatility Creates Supply Chain Uncertainties: The rubber industry faces persistent challenges from fluctuating raw material costs, particularly for synthetic rubber feedstocks like butadiene and styrene. Prices for these petrochemical derivatives can vary by as much as 40% year-over-year, creating budgeting challenges for manufacturers. Natural rubber prices are similarly unstable, influenced by weather patterns in major producing regions and speculative trading.

-

Technical Barriers in Specialty Applications: While commodity rubber products have reached manufacturing maturity, developing high-performance formulations presents significant technical hurdles. Advanced applications in aerospace, medical devices, and industrial machinery demand rubbers meeting stringent specifications for temperature resistance, chemical compatibility, and mechanical durability.

-

Environmental Compliance Costs Impact Profitability: Increasing environmental regulations present both challenges and opportunities for rubber manufacturers. Stricter emissions standards for synthetic rubber plants have required capital expenditures exceeding $500 million industry-wide for pollution control upgrades.

Opportunities Ahead

The global shift toward sustainable manufacturing and circular economy initiatives presents a favorable outlook. Regions worldwide are witnessing growing momentum through:

-

Waste rubber recycling presenting significant growth opportunities

-

Medical applications driving high-value innovation

-

Smart rubber technologies creating new application possibilities

Notably, major industry players have announced expansion strategies focusing on:

-

Advanced devulcanization technologies enabling material recovery

-

Development of medical-grade biocompatible elastomers

-

Integration of smart technologies with rubber products

📥 Download Sample PDF: https://www.intelmarketresearch.com/download-free-sample/1828/rubber-2025-2032-839

Regional Market Insights

-

Asia-Pacific: Dominates both production and consumption, accounting for over 70% of natural rubber output and 50% of synthetic rubber demand, led by Thailand, Indonesia, China, and India.

-

North America: Characterized by high demand for specialty synthetic rubbers like EPDM and NBR, with mature automotive sector accounting for over 40% of rubber consumption.

-

Europe: Shaped by rigorous EU sustainability mandates and circular economy policies, driving innovation in low-carbon footprint rubber solutions.

-

Latin America: Moderate growth constrained by economic instability but showing long-term potential through automotive sector development.

-

Middle East & Africa: Emerging player with growth concentrated in synthetic rubber production hubs like Saudi Arabia and South Africa.

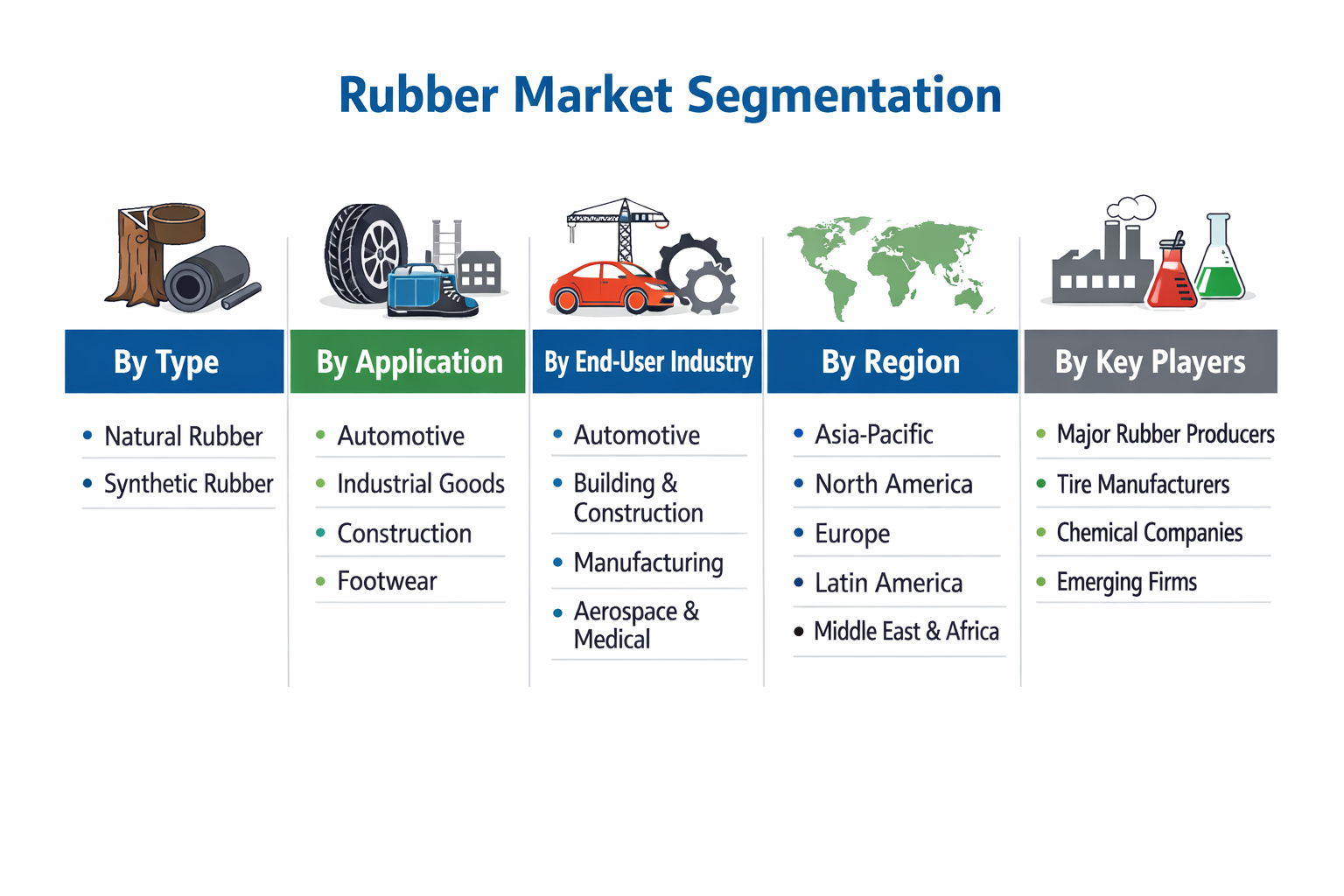

Market Segmentation

By Type

-

Natural Rubber

-

Styrene Butadiene Rubber (SBR)

-

Polybutadiene Rubber (BR)

-

Nitrile Butadiene Rubber (NBR)

-

Ethylene Propylene Diene Monomer (EPDM)

-

Others

By Application

-

Automotive

-

Building & Construction

-

Consumer Goods

-

Industrial

-

Medical

By End User

-

Tire Manufacturers

-

Industrial Product Manufacturers

-

Construction Material Producers

-

Healthcare Product Manufacturers

-

Consumer Goods Producers

By Region

-

North America

-

Europe

-

Asia-Pacific

-

Latin America

-

Middle East & Africa

📘 Get Full Report: https://www.intelmarketresearch.com/chemicals-and-materials/1828/rubber-2025-2032-839

Competitive Landscape

The global rubber industry exhibits a dynamic competitive structure, with major players operating across natural and synthetic rubber segments. Sinopec leads in synthetic rubber production with a diversified product portfolio catering to automotive and industrial applications. Meanwhile, Von Bundit and Sri Trang Agro-Industry dominate natural rubber supply chains with extensive plantations across Southeast Asia.

The report provides in-depth competitive profiling of key players, including:

-

Von Bundit (Thailand)

-

Sri Trang Agro-Industry (Thailand)

-

Thai Hua Rubber (Thailand)

-

Vietnam Rubber Group (Vietnam)

-

Sinopec (China)

-

Arlanxeo (Netherlands)

-

Kumho Petrochemical (South Korea)

-

ExxonMobil (U.S.)

-

Goodyear (U.S.)

-

JSR Corporation (Japan)

-

LG Chem (South Korea)

-

BASF (Germany)

Report Deliverables

-

Global and regional market forecasts from 2025 to 2032

-

Strategic insights into technological developments and sustainability initiatives

-

Market share analysis and SWOT assessments

-

Pricing trends and supply chain dynamics

-

Comprehensive segmentation by type, application, end user, and geography

📘 Get Full Report: https://www.intelmarketresearch.com/chemicals-and-materials/1828/rubber-2025-2032-839

📥 Download Sample PDF: https://www.intelmarketresearch.com/download-free-sample/1828/rubber-2025-2032-839

About Intel Market Research

Intel Market Research is a leading provider of strategic intelligence, offering actionable insights in chemicals, materials, and industrial infrastructure. Our research capabilities include:

-

Real-time competitive benchmarking

-

Global supply chain monitoring

-

Country-specific regulatory and pricing analysis

-

Over 500+ industry reports annually

Trusted by Fortune 500 companies, our insights empower decision-makers to drive innovation with confidence.

🌐 Website: https://www.intelmarketresearch.com

📞 International: +1 (332) 2424 294

📞 Asia-Pacific: +91 9169164321

🔗 LinkedIn: Follow Us